- The Hormuz crisis increases demand for West African oil, but it does not fundamentally shift global energy flows. Structural change in the oil market depends on long-term investment, not short-term disruptions.

- West Africa gains economic relevance as a diversification option, but production capacity and infrastructure remain limited. The region is viewed as a supplementary supplier rather than a replacement for established producers. Governance, political stability, and investment conditions will determine West Africa’s geopolitical role.

- Resources create opportunity, but institutions and regional coordination determine power.

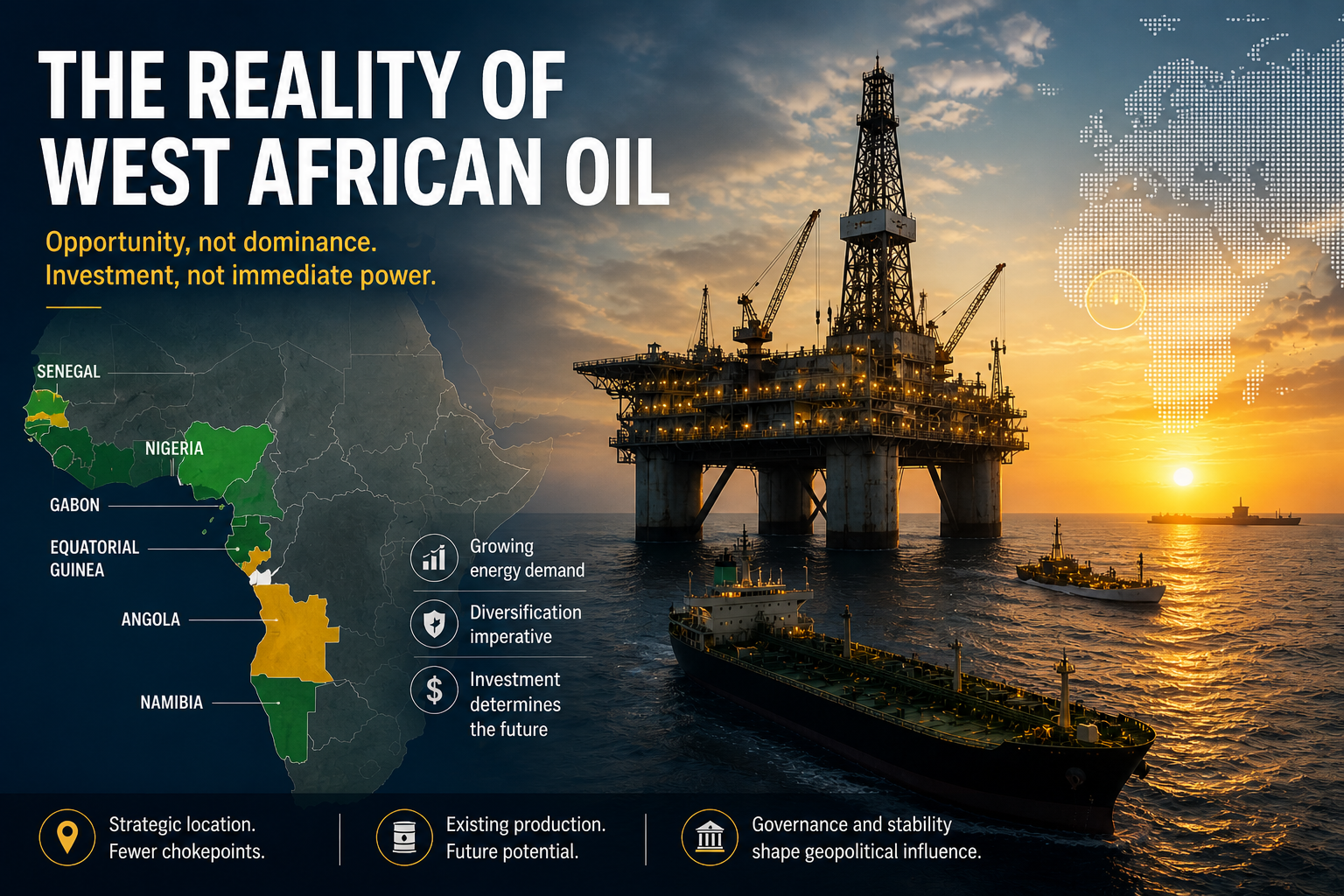

The Strait of Hormuz crisis has reminded Europe of its vulnerable position in the global oil market, shaped by strategic dependencies on a limited number of suppliers. Consequently, European attention is increasingly shifting toward African oil producers. These oil producing countries are mainly located on the Western coast of Africa. Producers potentially benefiting from this shift include Angola, Namibia, Gabon, Nigeria, and Equatorial Guinea. As Michel Don Michaloliakos (HIG) notes:

“West African states barely face any chokepoints in their supply of fossil fuels towards Europe, that is a significant strategic advantage.”

This advantage raises the central question of this article:

Will West Africa’s strategic advantages translate into lasting geopolitical influence in global energy markets?

The growing interest in West African energy resources reflects shifting strategic dependencies and evolving power relations within the global energy system. Whether this shift translates into geopolitical influence remains to be seen. Experts Jilles van den Beukel (HCSS), Michel Don Michaloliakos (HIG), and Wade Henckert (UNAM) offer their perspectives on this question.

Structural constraints limit the likelihood of a geopolitical shift towards West Africa

Despite the disruption caused by the Strait of Hormuz crisis, the conditions required for a structural shift in global energy systems remain largely unchanged. The oil market is characterized by capital-intensive infrastructure and long investment cycles. As recent analyses of global energy shocks demonstrate, the immediate response to supply disruptions mainly involves the rerouting of shipments, and implementing short-term policy measures rather than relocating production capacity. Structural changes in energy geography occur only when sustained shifts in investment flows follow these initial adjustments.

Given the temporary nature of the current disruption, a structural market change in which West Africa becomes the world’s primary oil and gas hub remains unlikely. As Jilles van den Beukel (HCSS) explains:

“The current disruption may last weeks or months, but it is unlikely to persist for years, given the importance of the region for global oil supply.”

Lasting market shifts occur when either demand or supply change significantly. The current disruption of supply leads to rerouting, and when issues persist, to geographical diversification in oil and gas investment. These investments characterize the oil and gas market, as oil and gas infrastructure requires capital intensive upfront investment, trust in the stability and investment climate is crucial. As Jilles van den Beukel (HCSS) explains:

“Therefore it is unlikely that a lasting reorientation of global energy flows will emerge from the current crisis. The Middle East and North Africa (MENA) region will remain central to global oil markets, and the economic incentives to maintain production in the region remain strong.”

Regardless of West African potential, the MENA region will remain the world’s oil and gas powerhouse. Significant capital investment would be required to expand West African production to levels capable of altering global energy balances The IEF estimates that a cumulative investment of $4.3 trillion will be needed between 2025 and 2030, which highlights the scale of the required capital. Wood Mackenzie notes that large projects can involve payback periods of 10 to 15 years and that scaling capacity can create delays and cost overruns, showing why these investments are both time- and capital-intensive.

Without a sustained increase in production capacity and infrastructure development, the region’s role in global energy markets will remain constrained by structural and economic factors. Structural shifts in the oil market occur only when investment flows change, which requires long-term stability.

Growing interest in West African energy resources reflect attempts at diversification of supply chains in order to reduce dependency on traditional producers. West Africa already is an oil-producing region. Output, however, remains modest compared with producers in the MENA region. Countries such as Nigeria and Angola together produce roughly 3 to 4 million barrels per day, compared with roughly 10 million barrels per day produced by leading exporter Saudi Arabia alone. Recent offshore discoveries in South western countries such as Namibia illustrate the region’s long-term potential, but translating these discoveries into production requires years of investment and infrastructure development.

The crisis increases the economic relevance of West African energy producers

While the Hormuz crisis is unlikely to produce a structural shift in global oil markets, it has nonetheless highlighted the strategic value of diversification in energy supply. Countries in Europe and Asia that rely heavily on imports from the Middle East are increasingly aware of the risks associated with concentrated supply routes. As a result, buyers are showing greater interest in alternative suppliers whose exports are less exposed to geopolitical chokepoints.

Recent market reactions to the Strait of Hormuz disruption illustrate how (South)West Africa’s position in the global oil market is perceived. Importers in Europe and Asia turned to West African oil as an alternative supply source. However, the export volumes did not surge, as traders held cargoes and production capacity remained limited. This illustrates the limited short-term flexibility of the region’s supply system. Furthermore, this suggests that international buyers see West Africa as a diversification option, but mainly as a supplementary supplier instead of a replacement for established producers.

Over the longer term, persistent instability in traditional supply regions may also influence investment decisions. International oil companies continuously assess geopolitical risk when allocating capital, and even small changes in risk perception can affect the relative attractiveness of different regions. Offshore projects in Africa may therefore receive additional attention, particularly if global demand remains stable and competing regions are perceived as less reliable.As Jilles van den Beukel (HCSS) observes:

“If geological potential is strong, investment can accelerate quickly once international companies see a viable opportunity.”

In this sense, the Strait of Hormuz crisis may enhance the economic relevance of West African energy producers without fundamentally transforming their geopolitical position. The region’s importance lies not in replacing established suppliers, but in serving as a complementary source of energy in an increasingly diversified global market. While higher prices improve revenues, they do not automatically create the stable investment climate required for large-scale production expansion.

Although the Hormuz crisis temporarily increases geopolitical risk in the Middle East, investors continue to view the region as relatively predictable due to its established infrastructure and regulatory frameworks, which remain key determinants of long-term investment decisions.

Hormuz crisis deepens existing issues and regional dynamics

The opposite could be argued about the West African investment climate. Large-scale energy projects require substantial upfront investment and long-term political coordination, both of which are difficult to secure in a region characterized by fiscal constraints and limited regional integration.

As Wade Henckert (UNAM) explains: “The lack of regional integration means that multinationals often dominate smaller African states.”Regional power dynamics further complicate the situation. Rising oil prices contribute to inflation, which disproportionately affects smaller economies that are dependent on oil markets. This can create new dependencies on stronger regional states. Furthermore, at the domestic level, oil discoveries generate political tensions. While rising prices put pressure on the population, expectations of future prosperity from oil revenues remain high. Governments seek to retain greater control over refining. An example is Namibia refusing TotalEnergies and Petrobras to acquire a major offshore drilling stake. The Namibian case offers an interesting example of the characteristics of the West African investment climate. Measures taken by the Namibian president, aimed at strengthening national control over resources, can signal political uncertainty to investors, reducing confidence in the long-term investment climate.

At the same time, geopolitical competition is intensifying. African governments increasingly diversify their partnerships, engaging more with China and Russia in mining and energy sectors. China has become a major investor in infrastructure and upstream energy projects across the continent, particularly in large producers such as Angola and Nigeria. Russia’s presence is more concentrated in security and political cooperation, especially in parts of the Sahel, with relatively limited direct investment in West African offshore oil. These relationships create economic opportunities while also introducing new forms of strategic dependence.

As Henckert (UNAM) argues:

“Africa has resources, but it remains divided, and its voice in global politics is limited.”

This illustrates the place of West Africa in the emerging new World order; the rich resources give the continent relevance, the lack of good governance, coherent regulation and stability limit the structural geopolitical influence of the region.

Conclusion

- Temporary disruptions do not automatically translate into structural shifts in global energy systems. Lasting geopolitical change requires sustained increases in production capacity and infrastructure, which are slow and capital-intensive to develop. However, already exporting West African producers such as Nigeria, Angola, and Equatorial Guinea will see short-term economic gains following the rise in oil prices

- Regional fragmentation and limited institutional capacity constrain Africa’s ability to convert resource wealth into geopolitical influence. Weak regulatory coordination and competition between neighboring states reduce bargaining power vis-à-vis multinational companies.

- Domestic political dynamics play a critical role in shaping the trajectory of oil development. Public expectations, inflationary pressures, and debates over local control of refining and revenues can create internal tensions that affect investment stability.

- The geopolitical significance of West Africa will depend less on resource availability and more on governance and stability. The geographical situation and resources create opportunity, but institutions determine geopolitical power.

- China is emerging as a major investor in infrastructure and upstream projects, mainly in Angola and Nigeria

- Russia is showing interest in Namibian uranium. Russian presence is mainly shaped through the Africa Corps in the Sahel and less in West-African oil.