The Belt and Road Initiative (BRI) remains one of the largest and most influential initiatives on the globe. Throughout its implementation, the BRI has been marked by substantial obstacles, ranging from widespread international backlash and criticism to the global epidemic, which triggered economic slowdowns and decelerated BRI projects and construction. Despite the pushback, Beijing persists with renewed aim to improve BRI engagements, fostering green-development through the Green Belt and Road, providing debt-sustainability support and allowing economies to benefit. The shift in approach creates a stark contrast between the 2010s and 2020s (post Covid-19 crisis), moving away from the grotesque lending-based engagements which characterised the first decade. To map out changes in China’s approach of the BRl, most important trends and the impact on global geopolitics, the reorientations should be highlighted and analysed, raising the question: What recent trends are apparent in the Belt and Road Initiative’s approach, and what does it mean for global geopolitics?

Key Motivations Behind the Belt and Road Initiative

Scholars widely debate the reasons for the BRI, however, ‘the reasons’ for the Belt and Road Initiative vary:

- The domestic need for natural resources to fuel the accelerated expansion of the Chinese economy;

- The shift in the global economy, requiring international competition;

- Preventing limitations on economic growth by increasing the scope beyond Chinese borders;

- Geopolitical factors, such as taking advantage of fluctuating stability in Western relations and reforming political relations in the rest of the world.

Besides these motivators, China aims to reshape global geopolitics and geoeconomics by reducing its vulnerability to Western-dominated trade routes and institutions. Beijing strives to assume a leading role in establishing international cooperation. Ultimately, the BRI reflects a blend of long-term geopolitical strategy and economic imperatives, allowing China to secure necessary resources and strengthen its influence while showcasing its development-model in contrast to Western-led models. Beijing aims to assume a leading role in establishing international cooperation standards.

Recent Trends

The Belt and Road Initiative experienced a shift from ‘quantitative to qualitative’ engagement. The shift was initiated after quantitative expansion became unbearable for the Chinese economy, leading to an economic slowdown. In 2023, the Third Belt and Road Forum for International Cooperation was held, where an eight-point plan was presented. The plan included four primary focus areas for the shift to quality:

- Redefining the scope of the BRI; Narrowing the list of prioritised countries

- Fostering positive attitudes towards China

- Increased digital engagements and expansion

- Shifting towards green economy

‘Small and Beautiful’ Projects

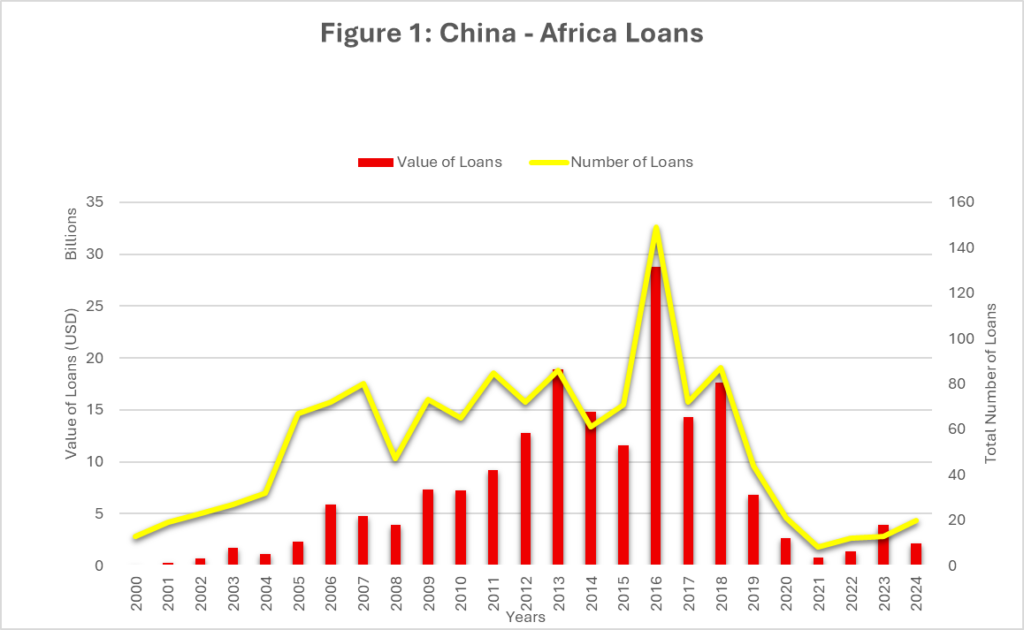

The shift away from large-scale projects, which characterised the early stages of the Belt and Road Initiative, towards selective, strategic and smaller-scale projects is apparent in Africa. The aggregate value of loans disbursed to Africa in 2024 was USD 2.1 billion, encompassing 20 distinct loan agreements. A total of 13 loans, valued at USD 3.9 billion, were issued in 2023, underlining the change in lending-approach. This contrast is strengthened when looking at earlier stages of BRI engagement activity and total loan-value. The year 2016 reflects the most active and significant engagement, with the total number of loans at 149, valued at USD 28.8 billion.

Boston University Global Development Policy Centre, 2026; Retrieved from http://bu.edu/gdp/chinese-loans-to-africa-database.

“The focus of China has shifted toward critical minerals, industrial capacity cooperation and tech cooperation, including on digital infrastructure, AI, green technology and remote sensing. “

– Dr. Yun Sun, Senior Fellow and Director of the China Program at the Stimson Centre

Improved Bilateral Trade Comes at a Price

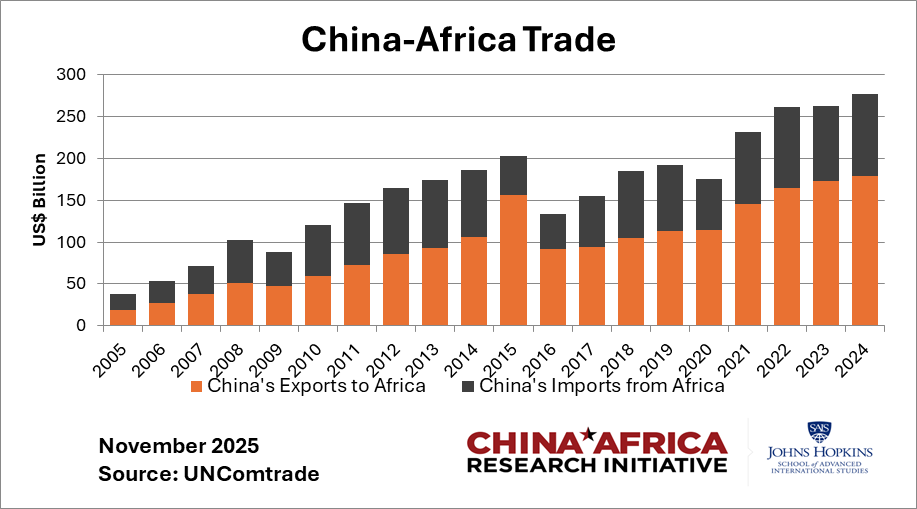

Along with a reduction in the intensity of large loans and projects, bilateral trade between China and Africa has significantly increased. As seen in the figure above, China-African trade is steadily increasing, reaching record highs of more than USD 348 billion in 2025. However, the significant trade-imbalance is evident. In contrast to the trade balance prior to the Belt and Road Initiative, the current trade balance heavily favours China. The increased bilateral trade is accompanied by a surge of African exports to China, mainly composed of natural resources; one of the large motivators behind launching the BRI. The high mineral exports to China could be explained by Resource-backed finance (RBF), which allows mineral-rich but capital-poor states to repay Chinese loans through mineral exports. This type of agreement is primarily seen in Africa.

“Technological cooperation is now the highlighted area, especially in terms of Chinese engagement. Africa remains to be a supplier of raw materials to China in terms of Chinese import.”

– Dr. Yun Sun

Mining vs. Processing Investment

Building on China’s need for natural resources, the BRI mining and metal investment statistics further underline Beijing’s interest. In 2025, the contrast between mining and processing engagements was quite stark, with mining investments at 61 per cent compared to 39 per cent towards exploitation. The Chinese approach to African minerals strengthens a highly dominant market position, as they hold stakes in crucial infrastructure networks linking African critical minerals to global shipping lanes. Chinese companies seek to ensure a foothold in Africa’s rich mining sector through various methods:

- Offtake agreements, which guarantee partnership regardless of future acquisitions;

- Acquisitions;

- Minority shareholding;

- Supplying Chinese technology and equipment in leasing deals;

- Farm-in contracts, funding exploration and receiving future production rights in return.

The raw materials China imports from Africa are fundamental for clean technology industries, in which China dominates. China is projected to provide 60 per cent of renewable energy capacity by 2030, because it manufactures over 90 per cent of the solar modules and 82 per cent of the wind turbines. China utilises its extensive foreign exchange reserves to meet recipient infrastructure needs while pursuing its own priorities.

The lack of local refining capabilities significantly impedes the effectiveness of the local economy, as the critical minerals could drastically transform Africa, given that they develop the downstream processing capabilities. Beijing’s commitment to upstream investment (extraction) compared to midstream investment (processing) is substantial. The imbalanced engagements allow for long-term extraction of raw minerals, with a slower-developing Africa as consequence.

“Mining and processing investments reveal a large gap in efficient development for the recipient states. These countries would gain substantial economic benefits from greater investment and construction in local processing capabilities; thus, the focus should shift towards building those capacities alongside extraction.”

– Michel Michaloliákos, geopolitical analyst for The Hague Institute for Geopolitics

Green Energy Development

China can pave the way in aiding developing countries towards greater, greener development.

“China mainly targets developing countries through BRI, primarily because most of the world’s countries are developing and because they have a demand for the infrastructure capacity that China can offer.”

– Frans-Paul van der Putten, Senion Research Fellow at Clingendael

Hence, green finance holds significant importance, particularly as targeting Low- and Middle-Income Countries (LMICs) involves addressing their economic and technological underdevelopment, alongside insufficient infrastructure to support the rapid growth of green energy to satisfy rising demand. Transition finance and green finance provide support to bridge the existing gap, allowing developing countries to step away from traditional (fossil) energy source dependencies.

The year 2025 evidenced the shift towards more energy-related investments; showed by the highest energy-related engagements since the launch of the BRI, totalling USD 93.9 billion, more than doubling the energy-related engagements of the year prior. China is pushing the shift to green through transition and green finance, further evidenced by the increasing green loans per year. In Q3 of 2025, green loans made up 16.09 per cent of the total outstanding loans balance, up from 8.2 per cent in Quarter 4 of 2021. A study on the effectiveness of green finance against environmental degradation stated that green finance has negative impacts on environmental degradation. Green finance bolsters regional mitigation of environmental degradation, resulting in a greener environment. In turn, a greener environment translates to improved sustainable growth and could enhance sustainable energy development.

Changed Approach to Lending

As the largest creditor of emerging markets and developing economies (EMDEs), China changed its approach in lending, developing numerous financial support instruments following the widespread debt-distress tied to the Covid-19 crisis. A pivot away from full-recourse sovereign debt transactions to non-PPG (non-public and publicly guaranteed, i.e. limited-recourse project finance) in transition mineral projects, highlights an important shift in approach as it circumvents immediate debt-pressure on governments.

Along with changed lending-approaches, Beijing leans towards financial support with smaller-scale infrastructure projects, often forgiving or rescheduling incurred debt on such projects. However, with larger-scale projects, China prefers to bankroll profitable projects, allowing the borrower to repay the debt.

Beijing promptly revisited its debt-sustainability measuring framework, making important changes to previous guidelines. The new guidelines provide:

- Shorter term for risk analysis (from 20 years down to 10 years)

- Broader eligibility by including LMICs

- Inviting (and praising) collaborative efforts with the IMF and World Bank.

The changes allow for a clearer understanding and overview of the debt-risks of loans through the shorter analysis-timeline, allow more BRI recipients to enter debt-restructuring negotiations, and allow other large creditors to provide feedback on Beijing’s debt-sustainability framework.

Final Reflection

The second decade of the BRI has seen substantial changes with implications for global geopolitics. Green- and transition finance coupled with the shift to ‘small and beautiful’ engagements allow for greater, greener and quicker development, besides providing debt-sustainability support through newfound lending approaches. The ‘backwards economic and technological levels’ of LMICs or LICs receive green finance along with abundant construction loans, providing significant short, and long-term benefits to the economy and environment. Beijing will set the standard for green cooperation, leading the way for clean-energy technology development in developing countries.

“But the absence of Global North for alternative support and sources of resources definitely does not boost confidence from Africa. Africa will be leaning more in favor of Global South for sure.”

– Dr. Yun Sun

Dominating the zero-emission technology market and production, while strategically strengthening their already-dominant-position in the midstream and downstream segments of transition mineral supply chains (e.g. raw material processing), China garnered substantial influence. Western dependence on low-emission technology (e.g. solar panels) and critical minerals creates a dependency on China, establishing a dominant position in geopolitics by creating vulnerabilities in opposing influences, furthering China’s geopolitical strength.