Anyone fixated on America’s trade offensive or theatrical military interventions is missing the Trump administration’s monetary Schlieffen plan. At the core of the dollar system a political struggle is currently unfolding between powerful factions of American capital. The stakes: who gets to keep collecting the rents generated by the dollar.

On one side stands rising techno-capital; on the other, the established financial elite.

That conflict is now playing out in the open. In a recent post on his platform Truth Social, President Donald Trump accused American banks of trying to undermine new crypto legislation and called for rapid progress on further regulation, arguing that the United States must become “the crypto capital of the world.”

To understand this struggle, this article looks at three developments: the integration of stablecoins into the dollar system, the rise of the crypto sector as a political interest group, and the legislative battle around new regulation such as the CLARITY Act — with implications for the American monetary system and foreign policy.

The “WhatsApp Moment” of Money — The GENIUS Act

This internal struggle has been triggered by the most recent American offensive on the international financial battlefield: the recently adopted GENIUS Act.

At the center of this law are so-called stablecoins — cryptocurrencies issued by private companies with the promise that they can be exchanged one-to-one for regular fiat money such as dollars. In doing so, stablecoins function as stable anchor points within the otherwise volatile crypto market. As crypto exchanges expand, their role in the global economy is increasing, particularly in developing countries where access to stable currencies is scarce. [1] [2]

Chris Dixon, crypto partner at Andreessen Horowitz, recently described stablecoins as the “WhatsApp moment of money.” Just as WhatsApp reduced the cost of international SMS messages to nearly zero, stablecoins push the cost and friction of cross-border payments toward zero.

While the law has already sent shockwaves through financial circles, it is still not fully recognized in public and intellectual debate for what it represents: a digital update of the dollar system, with potentially major consequences for the American financial system as a whole and for the monetary influence of the dollar.

Stablecoin issuers create tokens when users deposit dollars. The corresponding reserves are invested almost entirely in “safe” assets such as U.S. government debt.

With the GENIUS Act, Washington aims to provide further regulatory certainty to the stablecoin market while simultaneously “strengthening the American dominance of global finance,” according to President Trump.

Since the law was passed, the stablecoin market has grown from roughly $200 billion in 2025 to a peak of $317 billion in January 2026.

The legislation is meant to increase demand for U.S. government debt, push down interest rates, and strengthen the dollar as the global reserve currency “for generations.” Stablecoin issuers are therefore required to fully back their tokens with High Quality Liquid Assets — in practice mainly short-term U.S. Treasury securities.

Estimates for further growth of the stablecoin market range from $1 to $2 trillion in total market capitalization by the end of 2026 — a substantial boost for the American budget.

The Crypto Sector Gains Ground

The crypto industry is increasingly presenting itself as an organized capital faction within the American political economy. In the run-up to the GENIUS Act, major players in the sector poured hundreds of millions of dollars into lobbying efforts, campaign donations, and the financing of so-called crypto PACs. [3] [4]

With hundreds of millions spent on lobbying and campaign contributions, the crypto sector is pushing for a federal regulatory framework for stablecoins. Companies such as Coinbase, Ripple, and Andreessen Horowitz are openly positioning themselves as a new capital faction within the American political economy.

For market leaders such as Tether, the incentives are obvious. On the asset side of the balance sheet, U.S. government debt yields substantial returns.

In January 2026, Tether reported that it held more than $112 billion in Treasury bills, alongside tens of billions in short-term money market transactions backed by government bonds.

As a result, stablecoin reserves do not function as passive buffers but actively circulate within the core of the dollar funding system.

In practice, Tether operates as a large-scale liquidity manager within the U.S. money market and, through its Treasury holdings, has become one of the largest holders of American government debt in the world.

The interest income on these reserves generated more than $10 billion in profit in 2025 — more than banks such as ING — with margins reaching roughly 99 percent.

Even the Trump family itself has reportedly earned billions from its own crypto initiatives, with major investors in Trump-branded tokens gaining direct access to the president during a dinner organized at Mar-a-Lago.

What Is the Struggle About?

The best way to view the struggle over the dollar system is to think of different political jurisdictions as spheres of influence for financial actors. In that sense, the crypto sector has already conquered new territory — primarily in developing countries and within the crypto market.

Developing countries captured by the crypto sector

According to Chainalysis and the IMF, stablecoin growth is strongest in low- and middle-income countries, particularly in Sub-Saharan Africa and Latin America, where they are primarily used for remittances, protection against inflation, and access to dollars outside the formal banking system, especially in countries with high inflation and unstable national currencies.

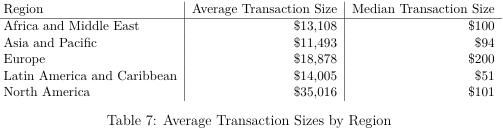

Although the IMF finds that the largest stablecoin flows in absolute terms occur in North America (around $633 billion) and Asia-Pacific (around $519 billion), flows relative to GDP are highest in Latin America and the Caribbean (7.7% of GDP) and Africa and the Middle East (6.7%), where usage is largely international in nature and focused on remittances and capital flight.

North America effectively functions as a net exporter of stablecoins and a source of global dollar liquidity, with stablecoin flows demonstrably increasing when local currencies weaken, inflation rises, and the dollar appreciates. The IMF study also concludes that Chinese stablecoin flows are significantly underestimated in commercial datasets, suggesting that the real inflows are considerably larger. Currently, around 99 percent of the stablecoin market is denominated in dollars.

Source: IMF

The CLARITY Act: The Battle for Developed Markets

After capturing the savings of citizens in developing countries, the crypto sector is now attempting to gain a foothold in the financial systems of developed economies.

The central issue now revolves around the CLARITY Act. As the name suggests, the law aims to bring greater regulatory clarity to cryptocurrencies and stablecoins. The legislation was expected to pass Congress last year but has stalled due to intense lobbying by both banks and the crypto sector.

The most controversial issue on the agenda: whether stablecoins should be allowed to pay interest.

The GENIUS Act explicitly prohibited stablecoins from paying interest. Yet through partnerships with crypto exchanges such as Coinbase it is still possible to earn returns of up to 3.5 percent (previously 4.5 percent). Technically these are not called “interest” payments but “rewards,” since interest is traditionally created through bank lending while these returns are backed by underlying reserves.

Banks are furious — and at the same time deeply worried. They fear that Americans will move their deposits to stablecoins en masse.

Their concern goes beyond lower profit margins on savings accounts. What is at stake is their position at the heart of the American monetary system.

Since the 1930s the system has been based on an implicit compromise: commercial banks create most of the money through lending, while the Federal Reserve sets the conditions and intervenes during crises. Household deposits form the stable foundation on which banks extend credit.

If savings were to shift to stablecoins on a large scale, more than just bank funding would change. Banks use savings deposits to extend loans to households and businesses. Stablecoin issuers do not: they invest the funds almost entirely in U.S. government bonds.

Money that would normally enter the economy as bank credit would instead flow directly into financing the American state. Banks would therefore lose not only a cheap source of funding, but also part of their role in credit creation.

This would represent a shift within what economists call “shadow banking”: financial institutions that perform bank-like functions without actually being banks. Yet even those systems ultimately remained connected to the traditional banking system and could rely on central bank support in times of crisis.

Stablecoins, in principle, sit outside that framework. They are issued by technology companies that are not banks and have no access to the Federal Reserve’s safety net. If such systems grow large enough, a crisis could eventually raise the question of whether the central bank should intervene to stop a run on stablecoins.

The stakes of the CLARITY Act are therefore less technical than they appear. At issue is whether stablecoins remain a complement to the banking system, or evolve into a parallel channel through which dollar liquidity is distributed outside the traditional banking hierarchy. Such a development would be a major blow to bank profitability, but it could also have significant consequences for the role banks play in money creation in the economy, and for the Federal Reserve’s ability to conduct effective monetary policy.

Europe’s Strategic Dilemma & Policy Recommendation

Warnings are now also being heard in Europe.

In its latest Financial Stability Review, the European Central Bank argues that strong growth in stablecoins could cause valuable retail deposits to flow out of eurozone banks. This would undermine an important and relatively stable funding source for banks, making their balance sheets more volatile.

The ECB also points to systemic risks. Two of the largest stablecoins hold volumes of U.S. Treasury securities comparable to those held by the twenty largest money market funds in the world. A sudden loss of confidence — a “run” — could trigger forced sales of these bonds, potentially disrupting the market for U.S. Treasuries.

This could also create problems for European banks if European savings migrate to American stablecoins. That would weaken Europe’s monetary autonomy.

This leaves Europe facing a strategic choice.

The digital euro could help protect European monetary autonomy in the digital age, but the current proposal of the Council of the EU remains cautious. Under the current design, the digital euro would pay no interest, and holding limits would apply to prevent deposits from leaving the banking system on a large scale.

That caution is understandable: banks play a central role in credit provision and money creation.

At the same time, an overly defensive design risks making the digital euro unattractive to consumers — thereby undermining its strategic purpose.

A possible middle ground would allow limited interest on digital euro holdings up to a certain threshold. That could encourage banks to offer more competitive savings rates — something that barely happens in countries such as the Netherlands, where savers have missed out on significant interest income.

At the same time, a gradual rollout combined with increasing holding limits could prevent deposits from abruptly leaving the banking system.

In addition, Europe could create space for euro-denominated stablecoins for international use, allowing public and private forms of digital money to complement rather than displace each other.

The digital euro is meant to strengthen Europe’s strategic autonomy. But if USDC yields roughly 3.5 percent and the digital euro nothing, Brussels appears to be hoping Europeans will keep their savings in a worse product for the sake of strategic autonomy.

What Now?

The outcome of this struggle may partly be determined in the upcoming midterm elections.

In a short period of time, the crypto industry has developed into one of the best-funded political forces in Washington. With nearly $200 million in campaign funding, the sector is attempting to secure its position in the legislative process around the CLARITY Act and further crypto regulation.

In the previous election cycle, this strategy already produced tangible results: a federal framework for stablecoins.

What is at stake in these elections therefore goes beyond the future of digital assets.

Congress is effectively deciding the institutional form of the American monetary regime. Will stablecoins become structurally embedded as a new pillar of the dollar system, or will they be restricted to protect the traditional banking system and existing power structures?

The real question is not whether the dollar will retain its dominant position, but through which infrastructure that dominance will be organized.

What is currently presented as technical regulation is in reality a renegotiation of power over liquidity, state financing, and the global circulation of money.

The midterms will reveal which coalition ultimately prevails.